Micro-Mechanics: Thesis has materialised

[Update] Micro-Mechanics (Holdings) Ltd. (5DD; MMH SP)

About (30 April 2026)

Share price: SGD 3.34

Market capitalisation: SGD 464 mn (USD 365 mn)

Enterprise value (EV): SGD 442 mn (USD 347 mn)

Average daily volume (ADV): SGD 1.5 mn (USD 1.2 mn)

LTM P/E: 34x; LTM P/B: 9x

My decision

This is a record of my investment decisions, not financial advice. Read the full disclaimer at the end.

I decided to continue holding my shares (previous: buy).

At SGD 3.34, 5DD shares now look fairly valued.

My investment has grown to a large portion of my portfolio. As a matter of prudent portfolio management, I plan to hold my shares while looking to redeploy the capital into new opportunities.

Background

What are my key takeaways from Micro-Mechanics’ earnings call on Wed 29 Apr 2026?

The cycle has turned. Revenue growth continued to accelerate. Operating profit margins continued to expand, finally recovering to the levels reached during the previous upcycle.

Near-term demand remains healthy. Management reported their lead time continued to increase. The risks of irrational capacity expansion remain low.

That said, there are indicators that we are no longer in the early stages of the upcycle.

Inventory growth finally increased faster than revenue. My framework suggests the current semiconductor shortage may end around calendar Q1’27.

I discuss these in detail in this post.

Business model

5DD’s financial year ends in Jun. Unless stated otherwise, all time references will follow 5DD’s financial year. For example, Q3’26 refers to Jan 2026 – Mar 2026.

If Micro-Mechanics (Holdings) Ltd. (5DD; MMH SP) is new to you, check out their business model here: Micro-Mechanics: After a +97% rally, is it too late to buy?

My reasons

Cyclical inflection

No longer in the early stage of upcycle. In Q3’26, inventory increased +23% YoY. This is the second consecutive quarter of YoY increase.

Management explained the increase was mainly due to higher material costs and 5DD building up inventory to support the fulfillment of confirmed backlog orders.

That the inventory (+23% YoY) increased faster than revenue (+16%) suggests we are no longer in the early stage of the current upcycle.

Risk looks low in the near-term. Management reported their lead time continued to increase. Demand still looks strong over the next year. The risks of irrational capacity expansion appear low.

Coupled with the positive industry read-throughs and healthy channel dynamics discussed in my thesis, near-term risks appear low.

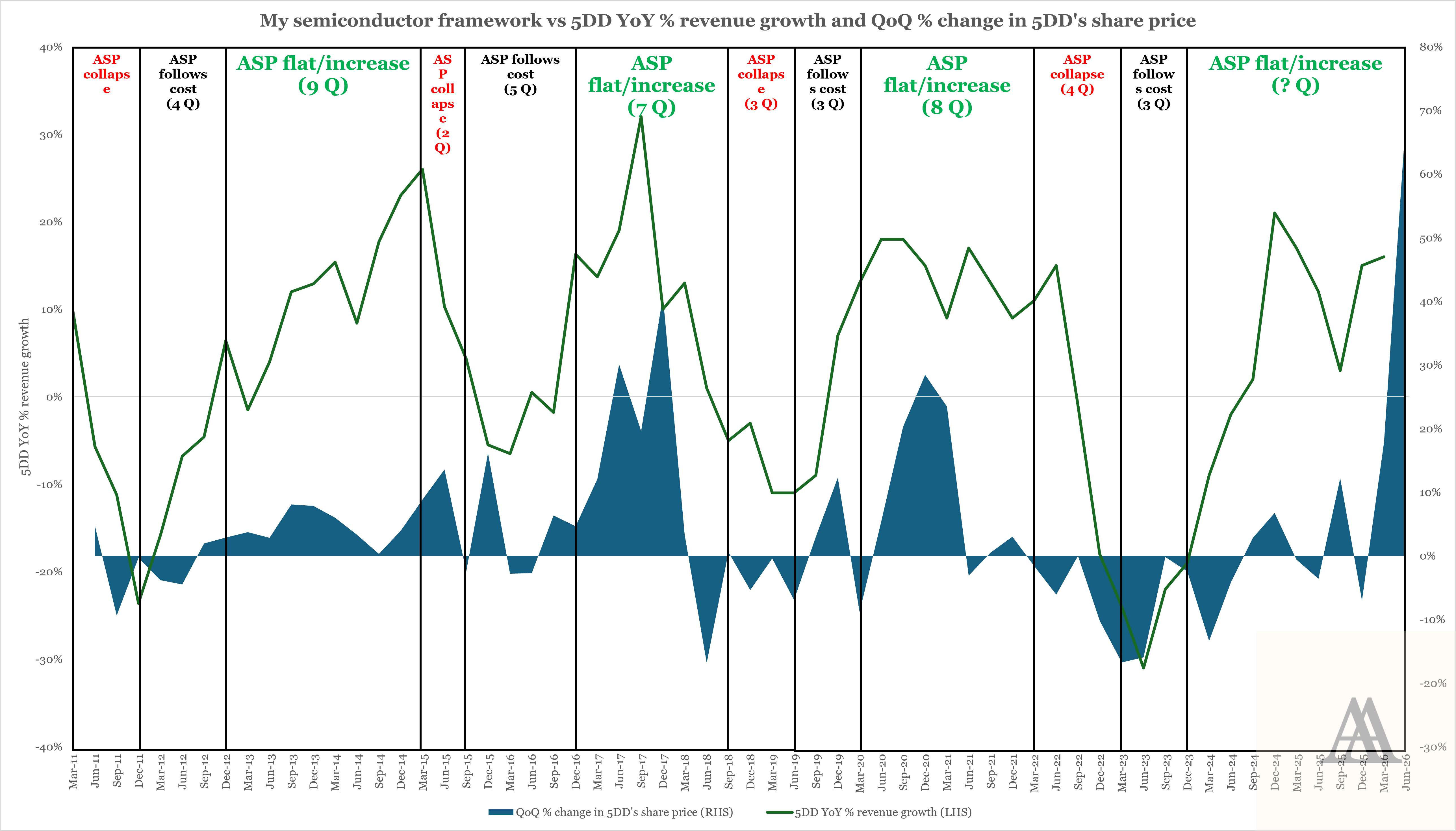

Potential downcycle from ~ Q3’27 (calendar Q1’27). For the reasons I discussed in my previous post, Where are we in the semiconductor cycle?, I believe the next semiconductor downcycle could start ~ Q3’27 (calendar Q1’27).

I will not repeat the explanation here. Instead, I will apply the framework to 5DD and show you the resulting chart.

Source: Angsana Anderson’s estimates; Tikr; Investing.com

5DD typically experiences revenue growth during memory chip shortage (when ASP flatlines or increases). These are also the periods when its share price rallies.

At the early stages of the current shortage, 5DD’s revenue growth was weaker than expected.

I suspect significant downstream inventories delayed customer orders. Inventory days at major OSATs like Amkor Technology, Inc. AMKR 0.00%↑ remained elevated during 2023 and early 2024.

When the memory chip industry flips to oversupply, ASP collapses towards cost. During these periods, 5DD’s revenue growth and share price typically decline.

In my previous post, I estimate that the current shortage will end around calendar Q1’27. If this is accurate, this means 5DD’s revenue growth could enter a downcycle from ~ Q3’27 (calendar Q1’27).

I am not betting on the exact timing. Of course, I expect my prediction to be off by one or two quarters, maybe even three.

Why, then, do I try to understand where we are in the cycle and forecast the next downturn?

It’s about positioning rather than perfect prediction.

After a huge rally, there is a natural bias to hold onto cyclical winners regardless of valuation. Recognizing that we are in the late stages of a shortage helps me overcome this bias.

It reminds me that current earnings are not sustainable, preventing me from extrapolating peak earnings.

Furthermore, this upcycle has caused semiconductor companies to grow into a disproportionately large part of my portfolio. Recognizing that a downturn is approaching pushes me to begin diversifying.

Prudent portfolio management. This is why I am looking to redeploy a portion of my capital from 5DD.

It is not because I have lost confidence in the company. On the contrary, 5DD’s management has navigated past downturns and capitalised on the current upcycle so well that the position has grown too large.

I believe 5DD has set a benchmark that many other public companies in Singapore would do well to follow.

Management continues to demonstrate strong alignment with minority shareholders. They maintain a high standard of disclosure, consistently providing important and candid insights into their business.

“A crucial test of management is whether they explain things clearly, honestly and transparently. Companies that succeed in this tend to be better run, in my experience.”

- Charlie Huggins, a former fund manager (20 lessons from 20 years of investing)

Other matters

Capex likely to increase. Since FY2022, capex has been running below depreciation. Management guided SGD 2.8 mn capex for FY2026. This will likely fall below depreciation (~ SGD 6 mn). Property, plant and equipment is now ~ 77% depreciated.

I asked whether they foresee the need to raise capex significantly above depreciation in the future.

Management explained they had been focusing on preventive maintenance. Going forward, they expect higher capex.

No loss of major customer. During the same period last year, 5DD reported 1 major customer that contributed more than 10% of revenue. 5DD did not report any major customer in this period.

Management explained there was no loss of business with this customer. The contribution from this customer fell below 10% because revenue from other customers increased.

Advance from customers not a meaningful leading indicator. Even though the amount is immaterial (~0.2% of revenue), I asked management to explain the nature of advances from customers. Does the company usually require customers to pay in advance?

5DD typically sells on credit. Sometimes, to manage credit risks in certain geographies, the company may require certain customers to pay in advance.

I believe this is why advances from customers does not show any meaningful correlation to revenue growth.

Factors that could lead me to increase investment in 5DD

Evidence that the current upcycle will be much stronger than historical cycles (e.g. current capex has not reached peak levels, the spread between ASP and unit cost of memory chip can continue to widen).

Share price falls > 30% without significant deterioration in business fundamentals.

Factors that could lead me to decrease investment in 5DD

Strong evidence that we are approaching the peak of the semiconductor cycle, and other investors are extrapolating peak earnings and overpaying for 5DD shares.

Upcoming events

Thu 27 Aug 2026: Q4’26 and FY2026 earnings release (expected)

Fri 28 Aug 2026: Q4’26 and FY2026 earnings call (expected)

Coming up next

Is there an opportunity in South Korea’s largest private education platform?

In Apr 2025, the company announced its corporate value-up program.

It planned to grow revenue by +9% p.a. and operating income by 19% p.a. through 2027.

The company also planned to increase capital returns to shareholders, targeting to return 60% of net income through dividends and share buybacks.

This implies 11% yield on enterprise value, an attractive 7.4% premium over South Korea’s 10-year government bond yield.

Finally, a catalyst is on the horizon. In Feb 2026, the media reported that management is looking to sell 32% of the company to private equity. The sale price would value the entire company at around KRW 925 bn.

Yet, the company is trading at only KRW 456 bn enterprise value and 5x NTM P/E.

What’s the catch?

Subscribe for free to be notified immediately when I publish.

Subscribe for 2 to 3 analyses of global SMID equities every week.

Discover overlooked ideas and rethink familiar names.

Published by Andrew Wong, ACA, CFA

Disclaimer

This publication is for informational, educational, and entertainment purposes only and does not constitute financial, investment, legal, or tax advice. The content herein is a record of my personal research and investment process, and all analysis, forecasts, and opinions expressed are solely my own.

I make no representation or warranty, express or implied, as to the accuracy, completeness, or timeliness of the information provided. The stock market is highly volatile, and my forecasts, estimates, and assumptions may prove incorrect.

I am not acting as your financial advisor or fiduciary. You should not rely on any information in this publication to make investment decisions. Under no circumstances will I be held liable for any direct, indirect, or consequential losses or damages arising from your reliance on the content of this publication.

At the time of publication, I hold shares in 5DD. I may change my views, predictions, or personal portfolio positioning at any time without notice.

Correction: Coming up next

"This implies 11% yield on enterprise value, an attractive 7.4% premium over South Korea’s 10-year government bond yield."

should be

"This implies 10.4% yield on market capitalisation, an attractive 6.5% premium over South Korea’s 10-year government bond yield."

Capital return to shareholders should be calculated based on market capitalisation, not enterprise value. Sorry